Consider the following spot interest rates for maturities of one, two, three, and four years.

Year | Rate

1 | 4%

2 | 5%

3 | 6%

4 | 7%

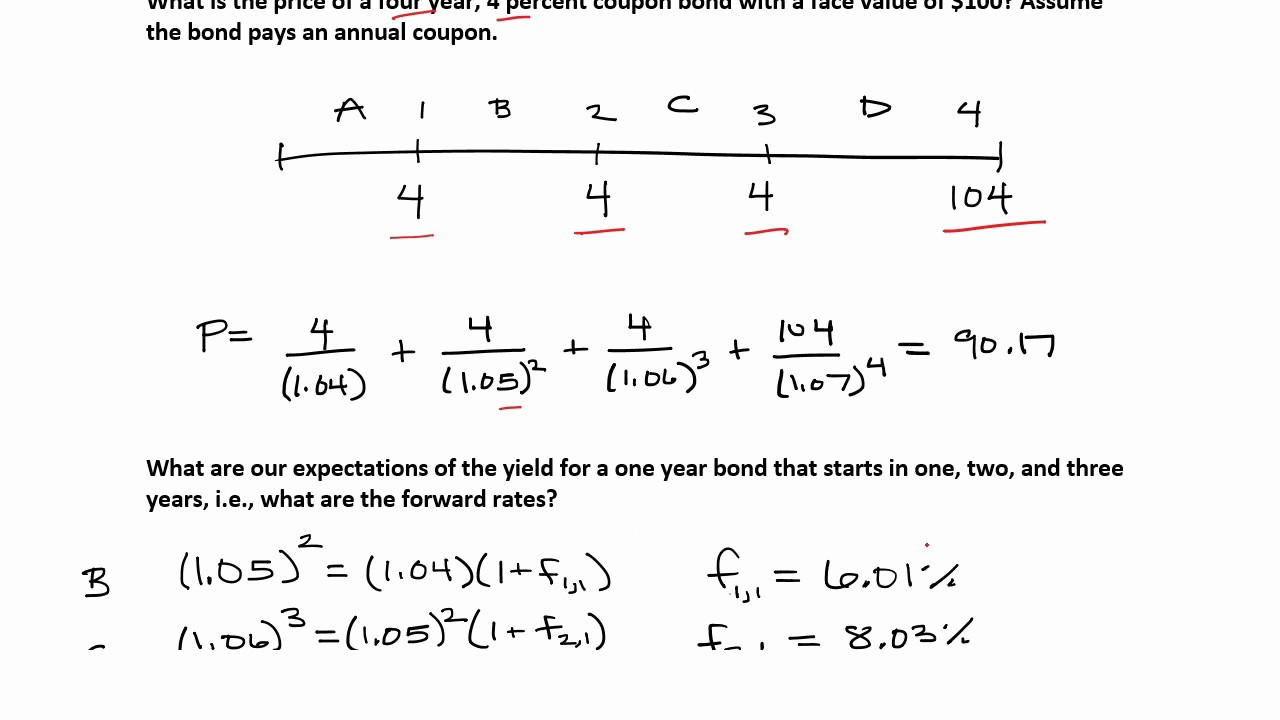

What is the price of a four year, 4 percent coupon bond with a face value of $100? Assume the bond pays an annual coupon.

What are our expectations of the yield for a one year bond that starts in one, two, and three years, i.e., what are the forward rates?

Suppose the inflation expectations are a constant 2 percent, what are the expected real interest rates for each one year period in the future?

Suppose that immediately after purchasing the bond that market expectations of the inflation rate decrease to a constant one percent. What are our new nominal forward rates? Assume expectations of real interest rates have not changed.

In one year, what do we expect the new term structure of interest rates to be?

In one year, what do we expect the price of the bond to be based on the new term structure of interest rates?

What do we expect the holding period return to be if you sell it immediately after receiving the first year’s coupon?

Note: There is a typo in calculating the holding period return. The correct formula is (92.22 - 90.17 + 4)/90.17 = 6.7%

Note: A pdf of the solution is available from here: [ Ссылка ]