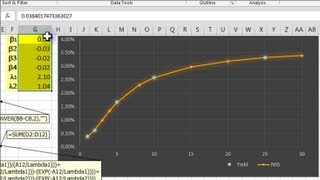

In this Excel Library video, we take a limited amount of bond yield information, and then extrapolate and interpolate from this a good-fitting yield curve which covers all the 'potential' rates in-between.

We do this using the Nelson-Siegel-Svensson method, via the Excel data tool, Solver, and minimise residual error squares to create a believable yield curve, despite a lack of complete information.

The main block of Nelson-Siegel-Svensson Excel formula code used in this video can be copied from here:

[ Ссылка ]

For financial education from London to Singapore and beyond, please contact MithrilMoney via the following website:

[ Ссылка ]

This MithrilMoney lecture was delivered by Andy Duncan, CQF.

Please read our disclaimer:

[ Ссылка ]